Posted March 27, 2026

By Matt Insley

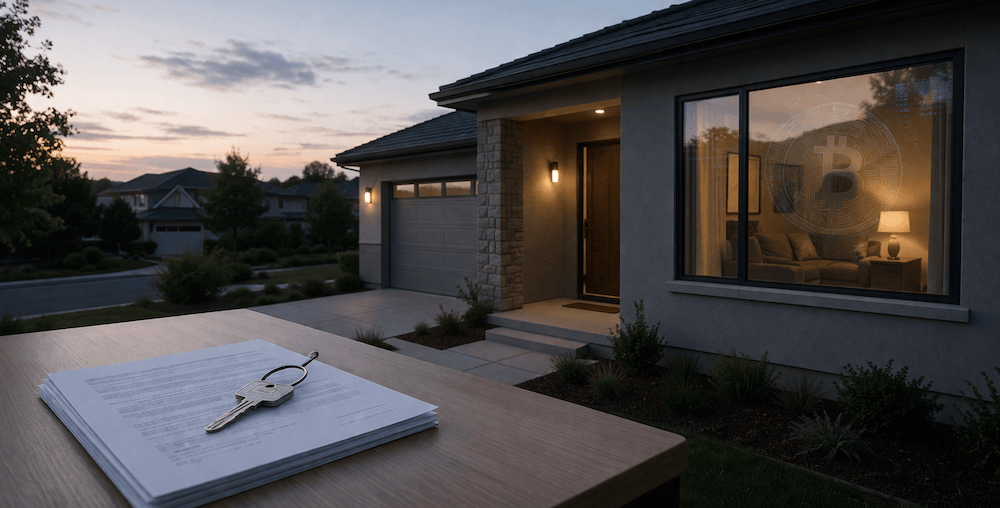

Fannie Mae Says “Yes” to Bitcoin

I’ve been staring at my mortgage statement long enough to know it like the back of my hand. Same bank. Same number, month after month. Same ritual (of mild irritation).

But something happened this week that made me look at that statement a little differently — and frankly, it made the whole concept of “buying a house” feel like it just got teleported about fifteen years into the future.

Coinbase and mortgage firm Better Home & Finance announced Thursday that Fannie Mae — yes, the $4 trillion government-sponsored enterprise that underwrites a significant chunk of America’s home loans — will now accept cryptocurrency-backed mortgages for the first time in its history.

The program allows prospective homebuyers to pledge Bitcoin or the USDC stablecoin as collateral for their down payment, without ever having to sell a single coin. (Other cryptos including Ethereum and Solana may be added down the road.)

As of Thursday, interested borrowers can sign up for early access at Better’s website. Here’s how it works…

Your Rundown for Friday, March 27, 2026...

Reading the Fine Print

A borrower can take out a standard 15- or 30-year Fannie Mae-backed mortgage through Better Home & Finance for a home purchase.

Then, instead of bringing a traditional cash down payment, they take out a second loan backed by their crypto — held in custody at a Better/Coinbase Prime account — to cover that down payment.

Both loans sit with Better, and the borrower makes one combined monthly payment. The crypto assets stay locked and can’t be traded, but critically, the borrower retains ownership and keeps any yield generated if they’re holding USDC.

Once the loan is paid in full, the digital assets are returned.

The no-margin-call structure is what caught my attention. Once the loan is issued, Coinbase and Better have essentially agreed to absorb the collateral risk for the life of the loan.

If Bitcoin drops 50%, nothing happens to your mortgage terms. No call. No forced sale. The lender can only move against you the same way any mortgage lender can — if you stop making your monthly payments for 60 consecutive days.

The tradeoff? You’re paying for it. Interest rates on the crypto-backed structure run about 0.5 to 1.5 percentage points above a standard 30-year loan, depending on borrower profile. (Plus, you’re servicing two loans simultaneously.)

Here’s the pitch: “People who are sitting on Bitcoin or USDC can put a roof over their head without needing to sell it, without needing to incur capital gains,” says Mark Troianovski, Coinbase head of consumer and platform business development.

Coinbase data shows 45% of younger investors own crypto, compared with 18% of their older counterparts — meaning an enormous chunk of would-be buyers are sitting on digital wealth they can’t easily convert to a down payment without a tax bill attached.

As a sweetener, Coinbase One members are eligible for a rebate worth 1% of the mortgage value, capped at $10,000. Other crypto assets like Ethereum and Solana may be added down the road.

Is this for everyone? Not even close. But for the crypto-native generation staring at a housing market that feels out of reach, this could be a bridge between digital wealth and the most traditional American asset of all.

The fact that Fannie Mae is the one stamping it legitimate? That’s not a minor detail. Zoom out further, and the systemic concern becomes hard to ignore.

The more crypto becomes accepted collateral in mainstream finance, the more a crypto crash becomes everyone’s crash — not just a bad month for speculators, but a contagion running straight through the housing market.

Fannie Mae carries an implicit federal backstop, and the stress-testing frameworks governing conventional mortgages weren’t built to absorb an asset class famous for 60% drawdown cycles.

It’s not that this product is necessarily a bad idea — it’s that novel financial instruments have a history of blowing up right after the government decides they’re safe.

Market Rundown for Friday, March 27, 2026

S&P 500 futures are down 0.25% to 6,500.

Oil’s up 2.10% to $96.55 for a barrel of WTI.

Gold is up 1% to $4,420 per ounce.

And Bitcoin’s pulled back 2.75% to $66,620.

Xi’s Zugzwang

Posted April 17, 2026

By Matt Insley

Orange Swan: Chaos Without Camo

Posted April 15, 2026

By Matt Insley

Boom for Whom?

Posted April 13, 2026

By Matt Insley

Delta: We Bought a Refinery

Posted April 10, 2026

By Matt Insley

1-800-CAL-MOVE

Posted April 08, 2026

By Matt Insley